The case is: The L/C stipulates:

45A: FROZEN YELLOWFIN TUNA

46A: INSURANCE POLICY/CERTIFICATE DULY ENDORSED COVER RISK AS PER INSTITUTE CARGO CLAUSES A WAR AND STRIKES AS PER INSTITUTE UP TO MAURITIUS CLAIM PAYABLE IN MAURITIUS WITH NO EXCESS.

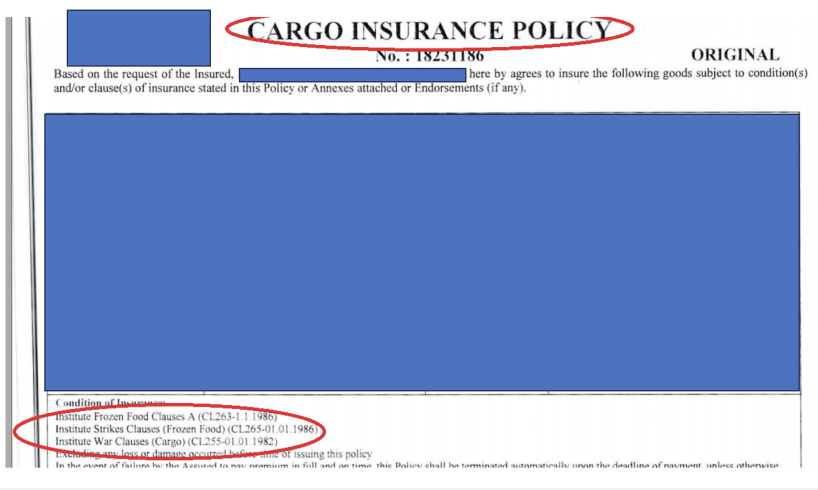

The presented insurance policy indicates condition of insurance:

This is a masked version of the document:

The issuing bank raised the discrepancy: Insurance policy: Clauses not as per LC “cargo clauses missing”

Is the discrepancy raised by the issuing bank valid?

Inmy opinion, this is a discrepancy. This is because the claim requires aninsurance document... "COVER RISK AS PER INSTITUTE CARGO CLAUSES A WAR AND STRIKES...".

The insurance document covers risks pertaining to the Institute WarClauses and the Institute Strikes Clauses but not to theInstitute Cargo Clauses (A).

Insuranceclauses are often difficult to understand for bankers and I agree that adocument checker is not an expertin insurance matters.

However, as theunderlying goods were frozen food (fish) it's "normal that the insurancedocument contains the moreapproriate" Institute Frozen Food Clauses A" which is in fact the"classic" II Cargo clause A, butfor frozen foods.

I know that a document checker should not investigate the content ofinsurance clauses, but I think that, content wise, this document reflects the required coverage.

I refer a.o. to several publications of experts inInsurance like: PowerPoint Presentation(clydeco.com)

https://abhillermarine.com/documents/clauses/institute-frozen-food-clauses-A.pdf

or the more extensiveand in-depth publication by Marsh

I'm quite surethat if the issuing bank would submit the presented document to the applicant /importer that the latter would gladlyaccept the document. In fact I wouldeven dare to say that the issuing bank wassomewhat careless or negligent when it issued its L/C knowing that the goodsare frozen food but, by routine(or lack of knowledge?),required a classic "allpurposes" ICC A etc.

Strictlyspeaking it's a discrepancy but a court would, after having heard insuranceexperts, reject such refusal....

Food for thought...

In my opinion,the discrepancy raisedby the issuing bank is not valid.

The L/C requiresInstitute Cargo Clauses A, War and Strike Clauses and the cargo under the L/Cis frozen food, hence, the factthat the insurance policy indicates Institute Frozen Food Clauses A, InstituteStrike Clauses and Institute War Clauses is deemed to meet the LC requirement.

Dear Emile,

Thank you very much for your comprehensive reply.

Theapplicant and the issuing bank could have been more precise with regard to therequest for insurance cover.

I agree with Nguyen and Emile.

Such a comprehensive reply by Emile.I have had occasions where the issuingbank would argue (that the discrepancy is valid). However, often when an ICC opinion is quoted or adocument (like the one provided by Emile) is referred to, the discrepancy is withdrawn.

Institute Cargoclause A and Institute frozen good clause A are not the same for the document examiner. Even for the court, the outcomeis uncertain. It depends upon how the proceedings will take shape.

I can refer here a very oldcourt case; J.H Rayner&Co Vs HambrisBank (not exactly similar to this one). Description of the goods in theL/C: Coromandel Groundnuts. The document mentioned description of the goods: Groundnut Kernels...

Before the court, thebeneficiary argued that anyone in thetrade would have known that the two descriptionsmeant the same thing. The court says, abank cannot be expected to have knowledge ofthe customs and customary terms of every one of the thousands of traders forwhose dealings it may issuecredits.

I personally "Thank my dear friend Emile" forenlighten me with this more appropriate frozen clause

A.Before that I was not aware of such clause. Had I issued the same L/C beforethis post, I would also have been inclined to ask for ICC A. What about You?

I think the beneficiary should carefully look into this clause andits ability to comply with it. If the beneficiary unableto comply, it should seek suitable amendment accordingly.

Firstof all, I’d like to start by saying I am very happy and honored to now be partof this Group of experts!

As a generic referenceto my background, I am Chairing the technical advisorygroup in ICC Finland.

I appreciate the thorough analysis from Emile, but I must say I amnot as confident as to how the court would actually rule it.

In any case, inthe context of checking documents under UCP 600, I don’t think that InstituteFrozen Food Clauses A would sufficethe requirement of Institute Cargo clause A simply because it goes beyond what is to be expected from adocument checker to know. On its face it looks like a discrepancy in myopinion.

Of course, no discrepancy.

Now, couldanybody tell me why, in 2023, bankers or applicants still require insurancedocuments to be endorsed? Aninsurance document is not a document of title and insurers don’t care about endorsement.

Incompetence? Ignorance?

Hi Daniel, Notignorance, but ISBP. See K19 and K21. If I understand it correctly, it is theright to receive payment("claims payable to"), not the full rights of an "insured"that are expected to be passed over be suchendorsed (at least it seems to me to be so under ISBP logic).

I am not aninsurance expert and do not know the practice in your country but the majorinsurance companies in my countryexpressly provide for the possibility to transfer the right to receive payment of claims by means of an endorsement(this being regardless of whether there is any mention of "to order" or not).

You could also see this as a matter of strict compliance versus common sense and good faith.

I would notrefuse these documents. The L/C asks for Institute cargo clauses A, theinsurance documents covers Institutefrozen foods clauses A. The ‘cargo’ in this case is frozen foods so the insurance document is more specific and, in my view,the required insurance for the cargo.

I want my doc-checkers to apply UCP 600 ofcourse but also touse their common sense and good faith.

Ifone would be more in favour of strict compliance, I don’t see how thebeneficiary could present a complying documentat all because I don’t understand the requirement:

“RISK AS PERINSTITUTE CARGO CLAUSES A WAR AND STRIKES AS PERINSTITUTE”

Asper institute what? Institute up to Mauritius. What does this mean? A good wayfor the issuing bank to refusein any case perhaps?

I’m awholehearted supporter of removing unnecessary payment obstacles caused by toostrict compliance. And I too advocate the approach to read the documents in context. But when it comes to insurance clauses It becomes a bit more delicatein my opinion

Would we then becomfortable with always replacing the word “cargo” with something reflectingthe nature of the underlying goods?And how to draw the line and/or give guidance to the document checkersin that respect.Also, the fact that ISBP 745 K18 specifically mentionsInstitute Cargo Clause

(A) as being one with “all risks” coverage, I think it is reasonablethat a doubt of the coverage occurs if itis altered in name. Interestingly also the presented document quoted “cargo” inone of the clauses and “Frozen foods”in others.

Having read the contemplations from both sides I dived a bit deeper into the InstituteCargo Clauses issueand am now more inclined to consider the insurance policyin question discrepant.

The reasoning is as follows:

We speak about Institute Cargo Clauses (A) (emphasis added) and not about mere "cargoclauses". I.e., InstituteCargo Clauses represent a specific set of contractual terms which is defined ina similar way as Incoterms - there is a set ofwritten paragraphs labelled as "Institute Cargo Clauses (A)".

I agree withthose saying that the L/C requirement was very purely drafted (it is quite hardto understand texts without correctpunctuation, to the very least) but still it is apparent that the L/C referred to Institute Cargo Clauses (A)and separately about "war and strikes". It did not refer to a specific version the clauses, hence any(such as CL252, 1/1/82, or CL382, 1/1/09, or any historical one could have been used), but it stillreferred to a set of clauses defined as "Institute Cargo Clauses(A)". To the contrary, InstituteFrozen Food Clauses (A), CL263, 1/1/86, represent completely separately definedset of clauses.

We can, ofcourse, ask why the issuing bank (or, hopefully for the issuing bank, theapplicant) called for aninappropriate set of clauses. But the L/C was issued in this way and itsrequirements must be met, no matter what.

It is a bitsimilar to the use of an "incorrect" Incoterm. I believe that all ofus who issue/advise L/C's and/or examinedocuments on a regular basis came acrossa situation where an apparently inappropriate Incotermfor the underlying transaction in question was used in the L/C (such as FOB forair transport, to mention probablythe most frequent situation; even FOB for containerised sea/multimodaltransport is not much of a suitableterm). But if the L/C is so issued, you must require "FOB" to appearon the invoice and you will notaccept "more appropriate" FCA instead arguing that it is apparent toanyone that FOB cannot be used for air transport.

Anything you can do is ask the applicantbefore issuance whether he really meansit. But if the applicant says "issue the L/C so because we have it so in ourcontract", most likely,you will not require that they change the contract (or insist on issuance of the L/C witha term conflicting with the contract) but you will issue the L/C including such an "incorrect" Incoterm.

Thus, in thesituation described in this query, in the shoes of a confirming / nominatedbank I would consider this issue as adiscrepancy and would refuse to honour or negotiate. For the issuing bank, I hope that they inserted this requirementon the applicant's instigation and NOT by their own decision (and I know that many banks use"standard" wordings, often including those similar to the one in question, by default without applicanteven knowing about that in advance). Were it on applicant's express instruction, the issuing bankshould refuse the document (and maybe learn the lesson and ask the applicant next time whether they wishto use a more appropriate clause). Were it the issuing bank's own default wording, I would be much morecareful – such unilateral deviation from the applicant's instructions might cause dispute not only with thebeneficiary, but also with the applicant.

In respect of:

+ UCP 600sub-article 14(d)

+ ISBP 745 paragraphC3, “There is no requirement for a mirror image”

+ document’s title being “CargoInsurance Policy”

+ document indicating “Packing: Container”

+ container being one of the three categories a general cargo issub-divided in I would reject the discrepancy mentioned by the issuing bank.

The questionis not if the documentis discrepant but if the issuingbank’s discrepancy is valid.

Dear Bogdan, the discrepancy is not very well drafted,either, but even here it is ratherclear what the issuing bank meant.

Bythe way, the issuing bank did not raise any discrepancy regarding bullet points3 to 5 in your latest e-mail. I.e., they did not questionthe nature of the documentor anything regarding containerisation.

Regarding thefirst two bullet points, in my reading UCP 600 sub-article 14 (d) ratherindicates that the document isdiscrepant (and the issuing bank's refusal valid) insofar as, on the reasoningI used earlier, it appears that"Institute Frozen Foods Clauses A CL263, 1/1/86" conflict with therequirement for Institute CargoClauses A required by the L/C. As you mentioned, there need not be a"mirror image" but there mustnot be conflict.

A discussion amongst the countryeditors.

Thecountry editors have been discussing the following issue. The below answers areexcerpts of the discussion.

The case is:

+ L/C description of goods:

15 units of xxx 10 units of zzz 5 units of ggg

... And description of goods (spareparts) goes on for other goods.

Partial shipmentallowed.

L/C does not show unitprices. Tolerance not allowed.

+ B/L of the 1st presentation shows the following:

"Partial shipment of 15units of xxx Total shipmentof 10 units of zzz"

+ B/L of the 2nd presentation shows the following:

"Partial shipment of 15units of xxx Total shipmentof 5 units of ggg"

The beneficiary’s bankdetermines that the B/L of the 2nd presentation is discrepant for over shipmentof xxx units (total 30 units) andasks the beneficiary to have the bill of lading corrected. However, thebeneficiary refused, claiming that 7 units of xxx were shipped with the 1st B/L and 8 with the 2nd.

Questions:

1/ Is the beneficiary’s bank correct?

2/ Are the bills of lading(that show partial shipment of 15 units of xxx) acceptable or must they showactual quantity of goods shipped?

In my personalview the bank must look at the B/L in context of the whole presentation. TheB's/L clearly suggest that they coveronly part shipment of the item xxx. If it is clear from the other documentswhat quantity of the item xxx was in fact delivered, the bank cannotclaim over shipment.

TheB/L need not contain detailed goods description. There is no requirement of UCPor international standard bankingpractice that the B/L show numbers of pieces or other units.B's/L usually contain

information about weight and volume, if such information conformswith the remaining documents, the B/L complies in this respect.

Wouldbe nice to know what the invoice and other documents show as goods descriptionand quantities of.

Nevertheless, in my opinion the bill of lading is discrepant. Thebill of lading must reflect what has actually been shipped.

We do haveISBP745 – paragraph C4 related to invoice, stating that “…invoice is to reflectwhat has actually been shipped,delivered or provided”. It is common sense to expect the transport document to evidence the invoiced goods descriptionand quantity of what has actually been shipped. If the invoice is allowed to show both goods descriptionand quantity stated in the L/C and goods description and quantity actually shipped, it is not the case when we are talking about the transport document.

There is something that I don’treally get. Eitherthe case was not properlypresented or ….

Under 1stpresentation the beneficiary’s bank had nothing to say about the bill of ladingwhich means that both invoice and B/L(and other docs if it is the case) show shipment of same quantity, i.e.,15units of xxx.

Under 2ndpresentation the beneficiary’s bank raised the discrepancy of over shipment butmade reference to B/L only, whichmake me think that the invoice does show shipment of only 8 units while bill of lading shows shipment of 15units. If the beneficiary’s bank asked the beneficiary to correct the B/L,did so because it shows a different quantity from the invoice.

Nomatter what quantity the invoice shows, it remains discrepancy of over shipmentbecause the full quantity of xxx was shipped and invoiced under 1st presentation.

Bottom line,there is something fishy here and, in my opinion, some necessary detailsare missing.

Agreed Radek … thisis the key text for me:

… B's/L clearly suggestthat they coveronly partshipment of the item xxx …

I revert with some clarification to not be misunderstood.

The bill of ladingdoes not have to show the quantityin pieces of each item shipped . Would have been enough to show goods description only .But since the b/l does show the quantities too, must not be in conflictwith what invoice evidenceto actually been invoiced and shipped.

You touchedthe key point in "must not be in conflict with what invoiceevidence". The crucialpoint is that the B/L clearly states that inrespect of goods xxx the shipment represents only a partial shipment. Neither UCP, nor international standardbanking practice require (except for invoice) that where the shipmentis indicated as partshipment, the document also showthe quantity actually shipped.

Therefore,in my reading of the situation there is no conflict, and the bank must lookinto the matter in context with the remainingdocuments in order to ascertain whether overshipment occurredor not.

This is not tosay that the description of goods on B/L is "fortunate". Were we inthe shoes of the beneficiary's bankwe would recommend him to show the actual quantity shipped as soon as we saw the first partial drawing. But as youknow, correcting bills of lading is not the easiest thing in L/C practice. Thus, the beneficiary may insistthat the B/L is correct issued in this way and, if his bank confirmedthe L/C and the presentation otherwise complies, that theconfirming bank pays.

Actually, the question was from a colleague. I asked that it isclarified if the quantity of goods shown on the invoicesare the same as that on the Bs/L and here is the information provided:

QUOTE

Commercial invoicesshow:

+For first shipmentidentical info that B/L:

"Partial shipment of 15 units of xxx Total shipment of 10 unitsof zzz"

+For 2nd shipment:

"Final shipment of 15 units of xxx Total shipment of 5 units ofggg"

UNQUOTE

I agreed thatthe bank cannot raise the discrepancy “over shipment” based on the informationon the B/L but let me know if theinvoices in question are discrepant when they show the quantity of goods as the above.

UnderUCP 600 and international standard banking practice the invoice must reflectwhat was actually shipped. Therefore, missing information on actual shippedquantity on invoiceis clearly a discrepancy.

Accordingto ISBP 745 paragraph C4 the description of goods on an invoice is to reflectwhat has actually been shipped.

For example,would have been ok for the invoicesto show:

+partial shipment of xxx: 7 units

+total shipment of zzz: 10 unitsAnd

+ final shipmentof xxx: 8 units

+ total shipment of ggg: 5 units

I do believe that must be a correlation between the description of the goods invoiced and the description of the goods shipped reflectednot only in the description itself but in the quantities and weights also and if ISBP 745 asks for thecommercial invoice to show what actually been SHIPPED (isn’t using the wording “not invoiced”) my understanding and believe is that a transport document, as the document that show what have been SHIPPED, must also evidencewhat actually been shipped.

Consequently, I still believe that the bill of lading should haveshown the actual quantity of xxx under each presentation.

Please read correct

(isn’t using the wording “invoiced”)

ISBP 745paragraph C4 relates expressly and only to the invoice. There is no requirementin UCP 600 and no suchinternational standard banking practice to require even any quantity stated ona transport document. It follows thatthe B/L would have been fully conform in this respect if it only had shown "xxx" and "zzz" (and,by the way, that is rather a common situation; very frequently there is no quantity detail on the transport documentother than gross weight (sometimes net weight) and volume and the documentonly states a generaldescription). See also ISBP 745 paragraph E22:

"A goods description indicatedon a bill of lading may be in general terms not in conlict with the goods description in the credit".

So, similarly aswith other "consistency" issues, you cannot look for a mirror imageand may only refuse documents ifthere is a conflict. There appears to be no conflict between the B/L and theL/C and even no conflict betweenthe invoice and the L/C. Thus, as to the B/L itself it appears to comply inthis respect.

However, if the description of goods is stated in the same way onthe invoice itself (i.e., only stating "partialshipment of 15 units of xxx" without stating actual quantity shipped, itis the invoice what is discrepant.